Grab a drink, sit back & get comfy! Shit’s about to get real. I’m always real but this is extremely vulnerable, and embarrassing. I’m gonna be talking about money management – or lack thereof might be a better way to say it. 🤷 This is a tough situation to see myself in. I know it’s dumb & something that could have been avoided. I can’t go back and change things. I can only go forward and take action to remedy the situation now…

Sidenote: Please don’t judge/be too harsh with your thoughts about me after reading this – I’m baring a lot here! 🙏

Recently, over at Me Skills, there was an expert money coach – Eileen Joy – who talked about Money Mindset: Fall In Love With Bossing Your Money Around. I wasn’t even there live but let me tell ya’ll – watching that replay, I felt called out! Or as I’m gonna rephrase it – called up, meaning it’s time to take action and fix things! They say ‘the teacher will appear when the student is ready’ and well, I (think) I’m ready!

Alright, let’s do this…

Money Management

I suck at money.

I suck at managing my money.

I suck at debt (as in staying out of it).

I suck at being aware of my finances (what’s coming in, what’s going out, how many subscription payments I have, how much credit card debt/payments I make every month, etc.)

I think you get the gist of what I’m saying. But before I talk about the present moment I feel like I need to take you back a few years (a lot of years).

How I Handled Money In The Past

This whole sucking with money thing has been an ongoing struggle my entire life. Back in 1993 & 1994 when I was in college (yea, I’m that old!), they handed out credit cards like they were candy… to a bunch of college kids that most of us didn’t even have jobs (like seriously did these companies not verify info?).

I applied & accepted every single one I had the chance to get my hands on and made a lot of stupid purchases – shopping sprees, food, and some college needs like pens, notebooks, etc.

The problem? The bills started coming in & I had no clue how I was going to pay them. So I did what any “smart” (that’s sarcasm if you didn’t catch that) 19-year-old would do – ignore them. I didn’t even bother opening them, instead just threw them into the trash!

Fast forward several years to 1999.

I was 24 & a single mom. The old debt from college was still hanging over my head (there is a statute of limitations on how long debt can be collected – 7 years – but the kicker is, it’s 7 years from the last time you made a payment/they had contact with you), but the credit card companies were starting to collect. One of the companies was garnishing my wages (don’t quote me on this but if I remember correctly, they were garnishing 35% of each paycheck).

I was driving a ghetto mobile (aka an old-ass car with a gazillion miles that breaks down every other day). And not surprisingly it breaks down again. Except this time, the mechanic delivers devasting news – it’s not fixable & no longer safe to be driving.

I needed a car to get back & forth to work (there wasn’t public transportation in the tiny ass town I lived in & my job wasn’t local). No bank would be dumb enough to give me a loan for a car so I did what any desperate single mom would do – went to a buy here/pay here place where they put me into a car, but it was just another ghetto mobile with tons of miles & problems.

Long story short – the transmission went after a few months and do you know the cost of getting a transmission replaced? It’s outrageous! And of course, the car was sold as is so I had no leverage in getting help from the car place to fix it.

So there I was yet again with another broken down car & no money to fix it plus still owed a shit ton of money on it. I once again made a really “smart” decision – just stopped making the payments. They came and repossessed the car.

Thankfully I was then given a car (if you’re wondering – yes, it was another ghetto mobile but it lasted for a while at least!) so I had wheels to get to work and around with.

The financial mess wasn’t getting any better. Instead, it was getting worse! On top of wages being garnished, I was then sued by a credit card company & the car place. This added even more debt because of court fees, costs, etc. I had no idea how I was going to get out of it so I sought out a credit counseling agency place where you would give them so much money each month & they would pay bills for you. My situation was so bad and I had so little income coming in they couldn’t even help me.

So I just kept robbing Peter to pay Paul month after month while my paychecks were garnished and all that jazz.

Somehow, things eventually got better & my situation changed.

Let’s fast forward many years now…

Money Management in my mid to late 30’s

It’s the end of 2015/beginning of 2016…

I’m quite a bit older but guess what? Yep, once again I found myself in the position of having an old broken down vehicle. And the mechanic had disappointing news – the cost to fix everything was more than the car was worth & he suggested it was pointless to fix.

I decided to try getting a car loan. I wasn’t expecting much when I met with the loan officer & wasn’t surprised when she told me I was denied but there was a solution – she could approve me if I had a co-signer (who had good credit).

Thankfully, I was smart enough to decline. I knew I would never ever put someone in that position of being responsible if something happened & I couldn’t make a payment.

Instead of fixing ghetto mobile #who knows (I’ve lost track by this time LOL), I decided to start looking for my dream car – a VW Bug. I knew the chances of finding one would be pretty slim because I only had $1,800.00 cash to work with to buy something.

Lo and behold my stepdad & I found one on Craigslist and went to test drive it. It was LOVE at first site. I knew I would buy it even before test driving it (even my stepdad after I purchased it, said he knew I was gonna buy it before I test drove it LOL). I will never forget the day I brought Ruby home! 😍 It was old. It had a LOT of miles on it. But it was my dream car!

Back when I had met with the loan officer, she made a suggestion of getting a secured credit card to help build/rebuild my credit. It took about a month but I eventually was able to put $500 on a secured credit card. After about six months of using that responsibly, a few bad credit credit card companies pre-approved me for their ungodly high interest rate $300 limit cards. I accepted two of them and used them responsibly for about six months.

Now, let’s move on into 2017…

Ruby, the dream VW Bug, was rollin’ along with over 200,000 miles on her but she had some issues & it was time to bid farewell to her. Off to the car dealership, I went! With a budget in mind (and hopes I could get approved for a car loan) I start looking. I purposely avoided the black VW Beetle I saw on the lot because I knew I wanted something bigger/roomier. But the salesman was like ‘have you ever driven a Beetle before? They’re roomier on the inside than the Bug.’ I decided to give her a drive and son of a gun it was love at first drive!

When I parked her, after test driving, I couldn’t wipe the grin off my face. I knew this was going to be my new car. Somehow. Someway. Inside we go to fill out the paperwork. As he faxes the papers over to my bank, I drive away holding my breath as I wait for him to call me back with the news.

It was 10 minutes before he closed for the day when he called…

I was approved for the loan but did need $1,200.00 as a down payment. Coincidentally, that’s exactly what I had in my savings account!!!

Probably not so smartly, I wiped that savings account out to put the down payment down and drove away with Morticia!

Here’s a Facebook post screenshot from that day – it was such a huge milestone for me I couldn’t help but share it!

And I then had to give her some personality:

This was the first time in my life I had a “new” vehicle. A reliable vehicle. A vehicle with less than 150,000 miles on it! It was so freaking exciting!

Okay okay enough gushing about Morticia (I still have her to this day – she has 119,000 miles on her & is going strong!). Let’s get back on track!

Over time, I built my credit up even more & was able to get a few store credit cards. Those helped build my credit even more.

Now, let’s fast forward to the present day…

How I Handle Money Today

We’re looking at 2023 now…

So how do I handle money today? I pretty much don’t. Or didn’t until recently! Sadly, today’s situation kind of feels like Déjà vu. The only difference this time around is the bills come in, get opened & paid. The problem? I’m only able to make minimum monthly payments and the interest is killing me – I make that monthly payment but as soon as they tack on the interest for the month, it’s like I didn’t even make a payment. 😭

Actually, let me backtrack for a minute…

I made a cross-country move in 2018. At this time I had several store cards (Torrid, Lane Bryant, Ulta Beauty & Kohls), my secured credit card from my bank, and 3 bad credit credit cards. More than I probably even needed, honestly. But suddenly I started receiving all these pre-approved credit card offers which didn’t bode well for me.

I would apply & accept the card.

Again.

And again.

And Again.

To the tune of:

Yep, that’s a STACK of credit cards! I’m not even going to tell you how many are in my hand. It’s ridiculous & this post is embarrassing & humiliating enough without giving an exact number of cards.

And almost every one of them is maxed out or close to being maxed out.

Like WTF was I thinking? 🤦🏽

Money Management Going Forward (And 6 Action Tips If You’re In Debt & Want to Get Out)

Because I don’t want this post to end with what feels like a doom & gloom vibe, I want to share 6 tips I’m putting into action to help get me out of this &#%!@?! mess.

But most importantly, I wanted to let you know that if you’re in debt (hopefully not a &#%!@?! mess like me!) you are NOT alone. Obviously, as you’ve just read my shit show of a messy situation… but look at this statistic:

Americans owe approximately $986 billion to their credit cards as of the fourth quarter of 2022?! (From a Forbes article)

That just proves we are not alone! Okay, onto the tips.

Tip 1: Assess Your Debt Situation

You have to understand the full scope of the situation before you can move forward and take action! And you can’t understand the full scope until you write it all down (put it in an Excel spreadsheet, etc. – whatever works for you) and see it up close & personal! Yes, it absolutely SUCKED doing this but it had to be done so I knew exactly how bad the situation was/is.

Tip 2: Create a Realistic Budget

For me, budgeting doesn’t even feel like an option at the moment because I have NO money to work with because everything goes towards debt. Last month, I had $17.37 left to my name at the end of the month after paying debt. How the hell do you make a budget with so much debt & not much income???

Tip 3: Prioritize Debt Payments

After getting everything all written down on a piece of paper I then reorganized & wrote everything on sticky notes so I could use those on a bigger piece of sticky note paper to move everything around. I organized them in order from the least amount owed to the most amount owed.

INSERT PIC HERE

Tip 4: Explore Debt Consolidation

I tried getting a loan through my bank to consolidate all debt into one payment. I was denied. I also tried a credit card that markets itself as being a balance transfer card & was denied there too. So clearly consolidating my debt is not going to happen, unfortunately, as this would be the best option for me (in my opinion).

Because I can’t consolidate the debt into one payment, I looked at the debt snowball and debt avalanche method. I’ve chosen to use the debt snowball method to pay my debt off.

Tip 5: Cut Back on Expenses

This tip sort of goes along with #1, at least it did for me. At the time I sat down to do #1, I also took a deep long look at ALL the subscription payments. You may not think, like I did, that $10 bucks here, $16 bucks there isn’t much but it really adds up!

This was fairly easy for me – I immediately cancelled probably 90% of the subscription payments I had. I was shocked at all the subscriptions I was paying for and NOT even using! This is what I cancelled:

- Hulu – $8.69/month

- Audible – $16.25/month (I hate listening to audiobooks – I like a “real” book I can hold in my hands)

- Amazon Music – $9.99/month

- Kindle Unlimited (I hate reading Kindle books – again, I prefer real books that I can hold in my hands!) – $11.99/month

- And several memberships I was paying for business-related things but could no longer justify the expense (there are a few I still have & I’m torn as to whether I should let them go or not).

I don’t do a daily Starbucks run so there’s no cutting expenses there. But I do have a favorite bagel shop, a coffee shop to work at (which means I buy at least something to drink every time I’m there), and a recent obsession – frozen yogurt. These are all expenses I can cut.

I don’t pay household bills (thank the lord for my man covering all those!) or else I would look at ways to cut household expenses.

One thing I have a note to do is call around to different insurance companies. I’ve been with State Farm since 2013 and I pay what people tell me is too much for full coverage insurance. If I can save money on this, that’ll be great.

Tip 6: Increase Your Income

I’ve been self-employed since 2006. I see and hear people all the time talking about how awesome self-employment is because they can earn whatever they want when they want. This hasn’t been my experience. My main source of income is my virtual assistant business. Income fluctuates a LOT and this is embarrassing to admit too – I am making the least amount of money now than I ever have as a VA! Well except for way back in the beginning when I started out and charged like $8/hour just to get experience & build my portfolio.

Income compared to previous years is at an all-time low.

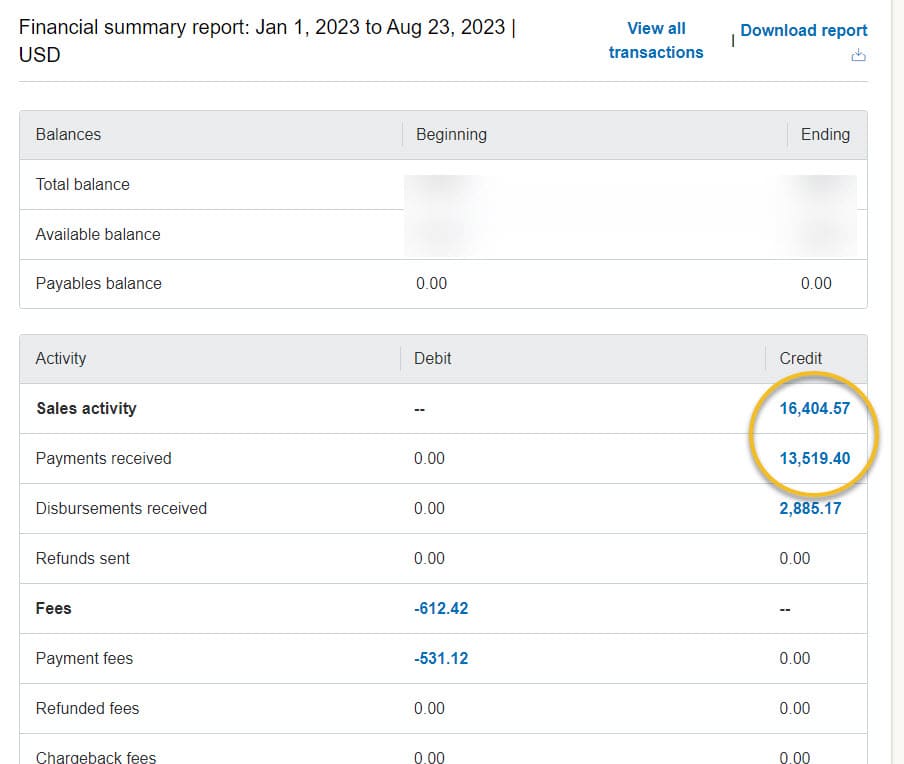

Here’s a look at this year (January 1, 2023 to August 23, 2023 PayPal Report) – All clients pay via PP:

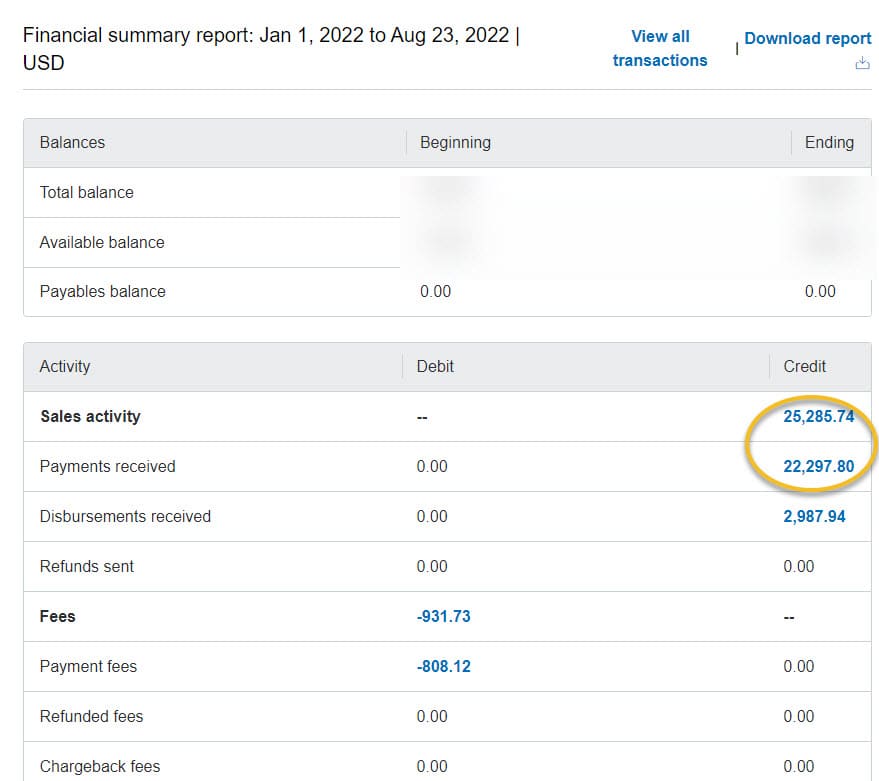

And now let’s look at a report from PayPal for the same time frame from last year, 2022:

I don’t understand why sales activity & payments received are 2 different numbers, though. But anyway…

This is a HUGE difference! And I feel it – I have a lot of the same debt from last year (credit cards, PayPal Credit & IRS – the IRS debt is definitely a story for a different day… sigh) + more (thanks to frequent doctor visits, blood work, and more, because of health stuff & no insurance) but way less income!

Part of that is because I love the current VIP clients I have and I don’t want to work with more clients (it may come down to it being a necessity that I look at bringing on some more clients though!). Instead, I want to continue working with them and focus on building income streams here at Shining Self – but to do that I need to get my head out of my ass and stop self-sabotaging myself & stop dragging my feet on some of the income-producing ideas I have.

I do have some things in the works for bringing in some cash somewhat quickly:

- Selling shelves, stands, etc. I don’t use/need in my office/house.

- Looking into Poshmark to sell clothes I no longer wear or have just been sitting in my closet for months and never worn!

- A side income from something I’m curious about & willing to play with for a bit to see how it goes but I’m not ready to talk about yet (if I ever even do!) 🤭

These 3 things won’t make me rich but any extra income that does come in from them will go towards debt and that’s a win in my book!

Why did I share all this? Maybe you’re thinking it’s crazy I did share all this – I get it, there are people that think I’m way too much of an open book! But the one thing I made a decision about back in 2018 was that I would no longer pretend to be someone I wasn’t & that if sharing my stories about things could potentially help even just one other person, then it was worth being vulnerable and sharing! That’s my WHY!

You are not alone!! This could have been me. I have not been good at credit cards. I remember getting a card with a $5000 limit in October and maxed it out for Christmas gifts by the end of November. I have had to remortgage my house a couple of times to cover my debts. Thank goodness I have paid off my mortgage and am paying down my credit cards, but like you I am taking a realistic look at what I am spending money on these days. It was quite a shock to see how all the "little" payments add up over the year(s). Thanks for sharing. It helps to know that I am not alone!

Fran, thank you so much for being vulnerable and sharing this with me & my community! It sucks knowing you were in this situation, but it also gives me hope that I too can get out of it! I am glad to hear you have paid off your mortgage & am paying down your credit cards!